However, there is a distinct difference between a generic online ballpark figure and an accurate, actionable insurance estimate.

To ensure you are getting the most realistic numbers without hidden surprises, here is a strategic guide to how vehicle insurance estimates are calculated, what variables move the needle, and how to audit your results.

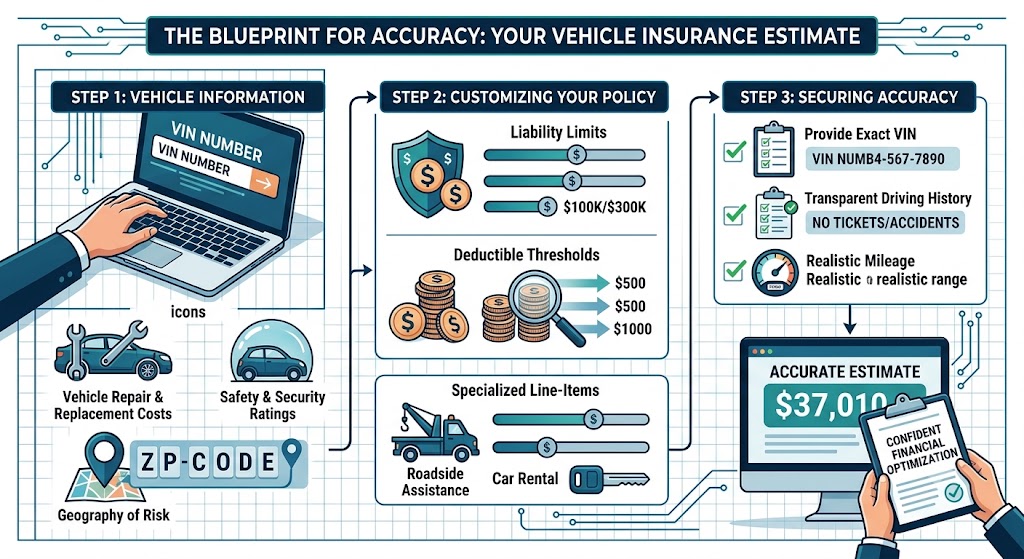

1. The Anatomy of a Vehicle Insurance Estimate

When an insurance carrier processes your data to generate an estimate, their algorithms evaluate your risk profile through two primary lenses: Who you are and What you drive.

Understanding how these pillars break down helps you see exactly where your money is going:

-

Vehicle Replacement & Repair Costs: The more expensive a car is to fix, the higher the comprehensive and collision estimates will be. Vehicles equipped with complex driver-assistance technology (like radar sensors in the bumpers or specialized windshield glass) naturally command higher premiums.

-

Safety & Security Ratings: Vehicles with high crash-test ratings and built-in anti-theft devices instantly trigger lower risk scores, driving your estimate down.

-

The Geography of Risk: Your zip code dictates local trends in traffic density, vehicle theft, vandalism, and weather anomalies (such as hail or flooding). An estimate in a quiet rural suburb will look vastly different from one in a dense metropolitan center.

2. Navigating Coverage Tiers: Customizing Your Estimate

An insurance estimate isn't a single, rigid price tag—it's a modular menu. When structuring your quote, you can actively manipulate your estimated premium by adjusting three fundamental layers:

Liability Limits

This is your financial shield against damage you cause to others. State minimums are rarely enough to protect personal assets. Adjusting your limits from standard minimums to a more robust structure (such as $100,000/$300,000/$100,000) ensures true security.

Deductible Thresholds

Your deductible is your out-of-pocket responsibility during a claim.

The General Rule: Increasing your deductible from $500 to $1,000 can reduce your monthly comprehensive and collision estimates by up to 15% to 30%. However, you must ensure you have that cash readily available in an emergency fund.

Specialized Line-Items

Don't overlook small additions that offer immense value. Roadside assistance, rental car reimbursement, and gap insurance (crucial if your car is financed or leased) add pennies to a monthly estimate but save thousands during a crisis.

3. Three Steps to Ensure Estimate Accuracy

To prevent your final, underwritten premium from skyrocketing past your initial online estimate, use this pre-flight checklist:

-

Provide the Exact VIN: Using a vehicle's make and model gives a generic estimate. Entering the exact Vehicle Identification Number (VIN) allows the insurer’s system to identify the precise trim package, safety features, and engine type, guaranteeing a highly accurate calculation.

-

Be Transparent About Driving History: Withholding a minor speeding ticket or a past fender-bender from the initial questionnaire will only result in an adjusted, more expensive rate later when the carrier pulls your official Comprehensive Loss Underwriting Exchange (C.L.U.E.) report.

-

Audit Your Annual Mileage: Be realistic about how much you drive. If your commute has shortened or you have transitioned to a hybrid work schedule, dropping your estimated annual mileage from 12,000 down to 7,000 can unlock significant low-mileage tier savings.

The Bottom Line

A professional vehicle insurance estimate is an active tool for financial optimization, not just a passive chore. By entering the process with accurate data, a clear understanding of your coverage goals, and a strategic approach to deductibles, you can confidently command the best rate the market has to offer.

Are you looking to run an estimate for a vehicle you already own to see if you can beat your current rate, or are you shopping around for a vehicle you plan to buy soon?