In the world of insurance, "motor insurance" is the broader umbrella that covers everything from your daily commuter car to motorcycles and commercial vans. In 2026, the market has shifted; while average premiums in many regions have stabilized after the record highs of 2024, the way insurers calculate your "risk" has become more high-tech than ever.

Getting a motor insurance quote isn't just about finding the lowest number—it’s about ensuring that when you’re on the side of the road at 2 AM, your policy actually shows up for you.

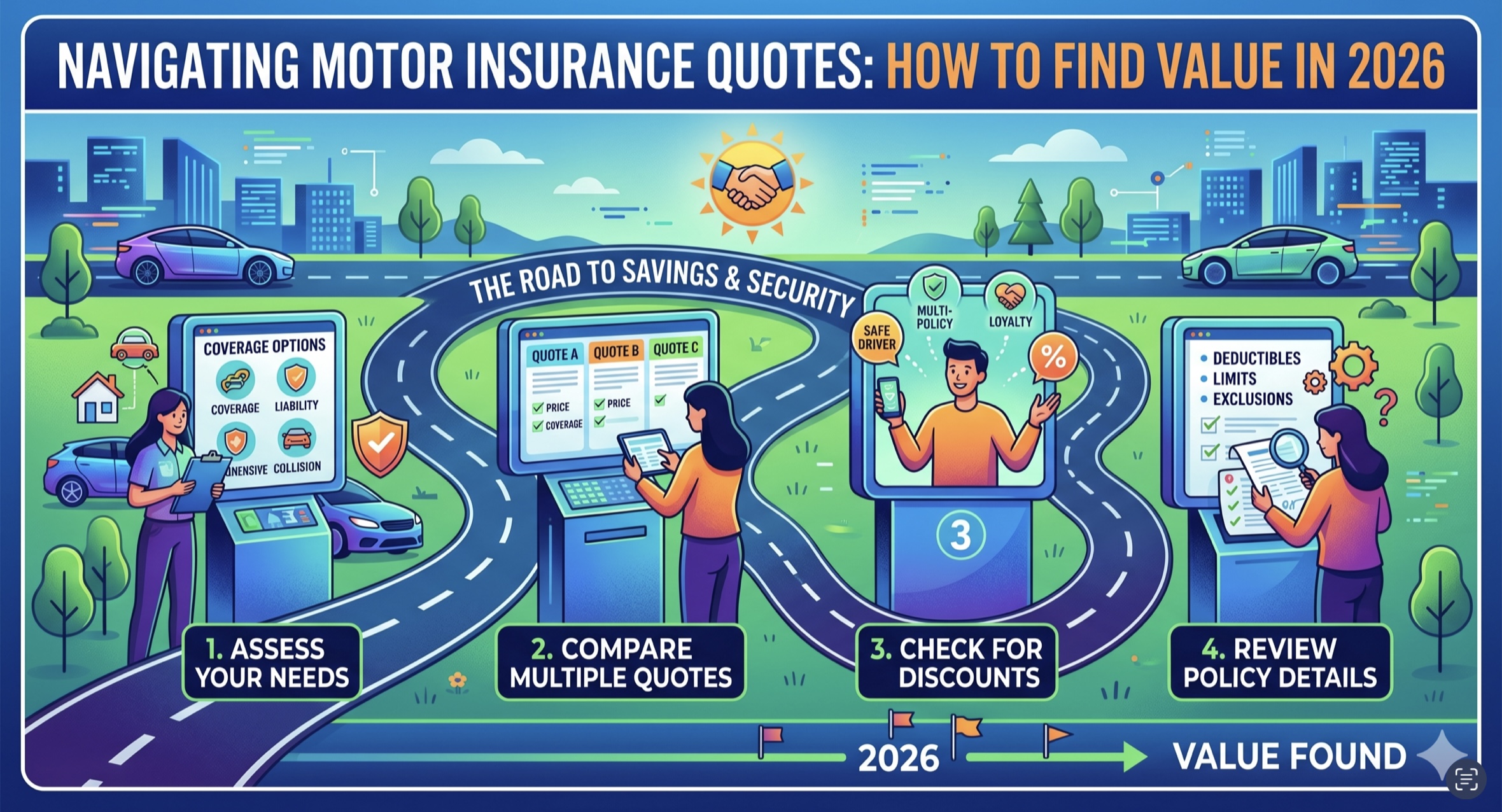

The Three Pillars of a Motor Insurance Quote

When you receive a quote, it is typically broken down into three main categories of coverage. Understanding these is the first step to a fair comparison:

-

Third-Party Only (TPO): The legal minimum. It covers damage to other people and their property but provides $0 for your own vehicle.

-

Third-Party, Fire, and Theft (TPFT): Everything in TPO, plus protection if your vehicle is stolen or damaged by fire.

-

Comprehensive: The "gold standard." It covers your vehicle for accidental damage, even if the accident was your fault, along with medical expenses and often "extras" like windshield repair.

Why Do Quotes Vary So Much?

You might notice a £200 or $300 difference between two companies for what looks like the same policy. In 2026, this is usually due to Smart Pricing factors:

-

Telematics (Black Box/Apps): Many insurers now offer "Pay-How-You-Drive" quotes. If you’re a safe driver, your quote could be 25–30% lower than a standard policy.

-

Vehicle Tech: Cars with advanced sensors (ADAS) are safer but more expensive to repair. Some insurers penalize these high repair costs, while others reward the safety features.

-

Regional Claims Data: Insurers now use real-time local data. If your neighborhood has seen a spike in thefts or floods recently, your quote will reflect that instantly.

How to Compare Quotes Like a Pro

To get a true "apples-to-apples" comparison, don't just look at the monthly premium. Check these three details:

Quick Tips for a Cheaper Quote Today

-

The "21-Day" Rule: Statistically, quotes requested 20 to 26 days before your current policy expires are significantly cheaper than last-minute renewals.

-

Job Title Tweaks: Sometimes, small (but honest) changes to your job description can lower your risk profile. (e.g., "Marketing Consultant" vs. "Sales Representative").

-

Increase Security: Adding a Thatcham-approved alarm or parking in a garage can trigger instant discounts on many motor quotes.

The 2026 Bottom Line: The cheapest quote is rarely the best value. Look for an insurer with a high "Claims Satisfaction Score." Saving £10 a month isn't worth a three-month headache when you actually need to fix your car.